In-Network vs. Out-of-Network: What’s the Difference?

Navigating health insurance can be overwhelming, and one of the most important distinctions to understand is the difference between in-network and out-of-network care. This choice can significantly impact your out-of-pocket costs, access to providers, and overall healthcare experience. Knowing how your insurance plan handles network coverage can help you make smarter financial and medical decisions.

What Is In-Network Care?

In-network providers are doctors, hospitals, and healthcare facilities that have contracts with your insurance company. These providers agree to pre-negotiated rates, which makes care more affordable for policyholders.

Benefits of In-Network Care

✅ Lower Costs – Because of negotiated rates, co-pays, deductibles, and overall medical expenses are typically lower than with out-of-network care.

✅ Simpler Billing – With in-network providers, billing is usually more predictable, reducing the risk of surprise medical bills.

✅ Easier Insurance Processing – In-network providers are more familiar with your insurer’s claim procedures, leading to fewer delays or denied claims.

Most insurance companies provide an online directory where you can check which doctors, hospitals, and specialists are in-network before making an appointment.

What Is Out-of-Network Care?

Out-of-network providers have no contract with your insurance company, which means they can set their own prices. Without negotiated rates, your insurer may cover only a small portion of the bill—or none at all—leaving you responsible for the remainder.

Downsides of Out-of-Network Care

❌ Higher Costs – You may be responsible for paying the difference between what the provider charges and what your insurance covers, a practice known as “balance billing.”

❌ Unpredictable Expenses – Without set pricing agreements, out-of-network care can lead to unexpected and substantial medical bills.

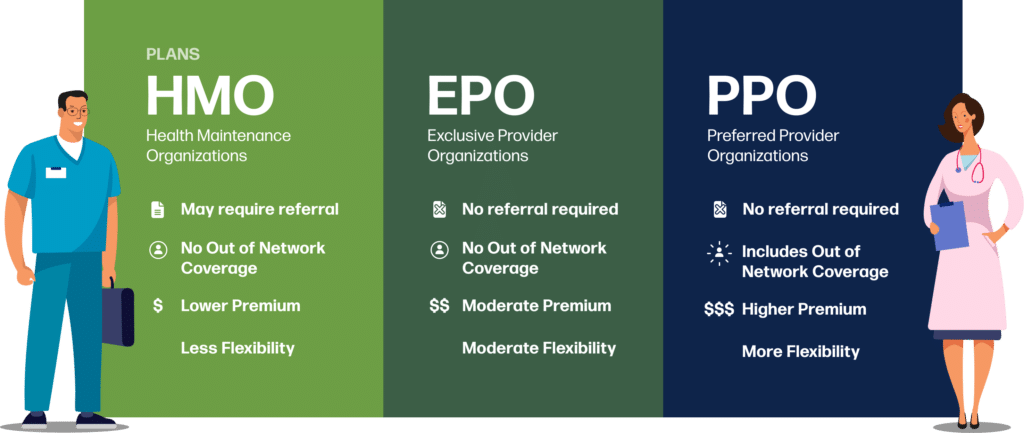

❌ Limited Insurance Coverage – Some plans, like HMOs, do not cover any out-of-network care except in emergencies. Others, like PPOs, may offer partial coverage but at a much higher cost.

While avoiding out-of-network providers is generally recommended, there are cases where you might need to seek care outside your network—such as emergencies or specialized treatments not available in-network.

What If Your Doctor Is Out-of-Network?

If your preferred doctor is out-of-network, you still have options:

- Pay out-of-pocket – While expensive, this allows you to continue seeing your preferred provider.

- Negotiate a cash rate – Some doctors offer discounted self-pay rates if you’re paying without insurance.

- Request an exception – If no in-network provider offers the care you need, your insurer may approve an out-of-network doctor at in-network rates.

- Switch insurance plans – If your doctor is out-of-network, consider switching to a plan that includes them during open enrollment.

Emergency Care and Out-of-Network Costs

In an emergency, you may not have time to check whether a hospital or doctor is in-network. Fortunately, most insurance plans provide some level of coverage for out-of-network emergency care.

Additionally, laws like the No Surprises Act help protect patients from excessive charges in emergencies, preventing hospitals from sending large balance bills for out-of-network care. However, it’s still important to follow up with your insurer after an emergency to understand your coverage.

Choosing the Right Health Plan

When selecting a health insurance plan, consider the following:

✔ Are your preferred doctors and hospitals in-network? Check the insurer’s provider directory before enrolling.

✔ How often do you need care? If you see doctors frequently, an HMO with strong in-network coverage may be a cost-effective option.

✔ Do you need out-of-network benefits? A PPO plan may be better if you want flexibility to see specialists or providers outside your network.

✔ What are the total costs? Compare premiums, deductibles, co-pays, and out-of-network fees to ensure the plan fits your budget.

Final Thoughts

Understanding the difference between in-network and out-of-network care is essential to managing healthcare costs and avoiding financial surprises. Always check a provider’s network status before receiving treatment to prevent unexpected bills. Being informed and proactive about your insurance choices can help you make the most of your healthcare coverage while keeping costs manageable.

Get Started Today

Getting More Money into YourPocket Starts With Your Inbox!

Create a free account with YourPocket, and get tools you need for financial freedom and control.